Slippage in the Stock Market: The Hidden Profit Killer

Hi Stratzy users ![]()

A lot of times, we focus heavily on signals, entries, and strategies but completely ignore price deviation during execution.

That small gap between deciding to trade and actually getting filled slowly eats into performance.

Over time, these “small” deviations compound.

And that’s where returns quietly leak.

What is Slippage?

Slippage is simply the difference between the price you expect and the price you actually get.

Example:

You decide to buy a stock at ₹100.

By the time you place and execute the order, price moves to ₹102.

You’re filled at ₹102.

That ₹2 difference is slippage.

For manual traders, slippage is usually higher.

In automated systems (algos), it can be measured, controlled, and optimized.

A Real Options Example

Let’s say you’re buying 100 lots of Nifty 25k CE at ₹50.

Mid-execution, the market jumps 5 points.

You get filled at ₹55.

That’s:

₹5 extra per lot

₹5,000 extra cost

On a ₹5L trade → 1% slippage instantly

Now imagine this happening daily.

During extreme events:

2020 COVID crash

2010 Flash Crash

Stops slipped 20–50% worse due to:

Thin market depth

Panic

High volatility

In India:

Liquid stocks → ~2–5 paise average slippage

Illiquid stocks / post 3 PM → 20–50 paise slippage

Same strategy. Very different outcomes.

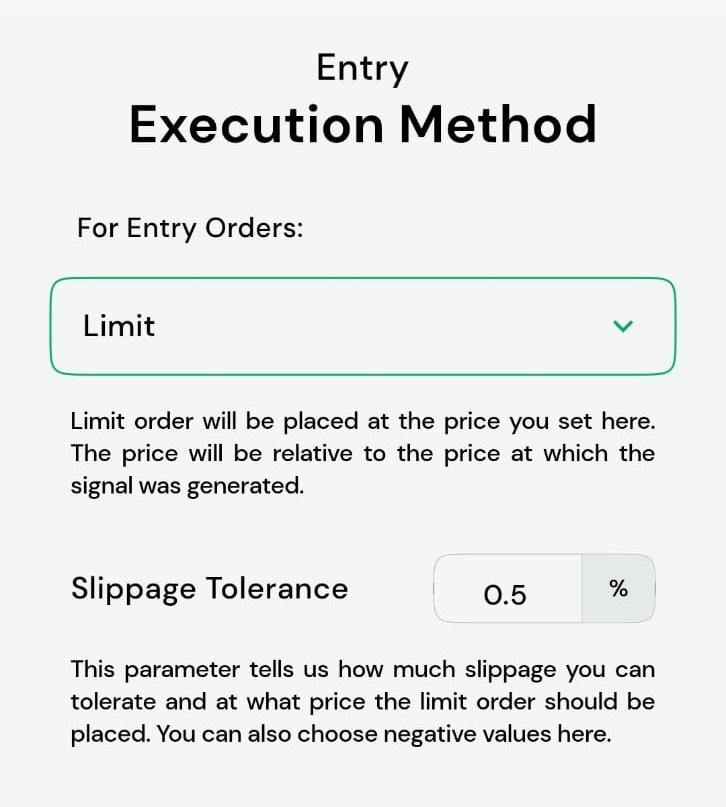

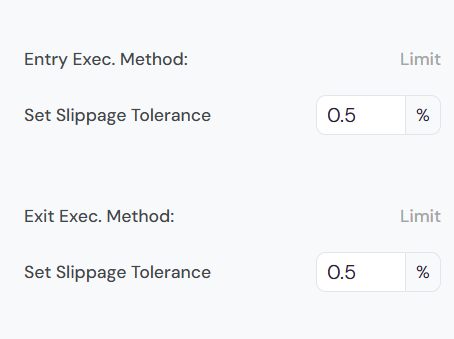

How to Minimize Slippage (Stratzy-Specific)

This is where execution matters.

-

Prefer Limit Orders

Market orders chase price.

Use limit orders instead place them 5–10 paise inside the spread.

Stratzy’s algo editor lets you enforce this easily. -

Trade During High Liquidity

Best window: 9:30 AM – 2:00 PM IST

Avoid:

Market open chaos

Closing hour

Muhurat trading

- Avoid Event Volatility

RBI policy

Earnings

FII data dumps

Use the NSE calendar inside Stratzy.

Pause bots 15 minutes before and after events.

-

Set Slippage Tolerance

Even if you use market orders, Stratzy allows you to define acceptable tolerance.

This puts a hard cap on bad fills.

Final Thought

Slippage isn’t loud.It doesn’t show up in strategy logic.But it quietly kills PnL.

A lot of trading is not just what you trade but how fast and how cleanly you execute.

That’s where algos shine.

They don’t hesitate, don’t chase, and don’t panic.

Slippage is a hidden cost.

Execution is the edge.