Thanks to our community members who keeps asking thoughtful questions around risk and performance.

One concept every investor and trader must understand is drawdown.

What is a drawdown?

What is a drawdown?

Think of your portfolio like trekking up a mountain.

-

You reach a peak

-

Then the path dips before climbing again

That dip from the highest point to the lowest point before recovery is called a drawdown.

In simple words:

Drawdown = temporary loss from your previous high

In trading, this can mean real losses in the short term.

But over the long term, the true outcome of a strategy is visible only after it completes multiple market cycles.

It is not a permanent loss but it tests patience, discipline, and risk tolerance.

Why drawdowns are inevitable in trading ?

Why drawdowns are inevitable in trading ?

No strategy in the world goes up in a straight line.

Even if:

-

Long-term returns are strong

-

The strategy is statistically sound

-

Risk management is in place

Markets move in cycles:

-

Volatility regimes change

-

Correlations spike suddenly

-

Short-term randomness dominates

![]() Drawdowns are not a sign of failure. They are the cost of participation.

Drawdowns are not a sign of failure. They are the cost of participation.

The key question is not “Will there be a drawdown?”

The real question is “How deep will it be and how long will it take to recover?”

This is where recovery time (or recovery days) becomes just as important as the drawdown percentage and why smoother portfolios matter in real life. We showcase this in algos section as well

How should you interpret drawdowns?

How should you interpret drawdowns?

In the below image, both investments end at similar returns.

But:

-

One path is smoother

-

The other has deeper and sharper drawdowns

![]() Same destination. Very different journeys.

Same destination. Very different journeys.

For most investors, the smoother journey:

-

Is easier to stay invested in

-

Reduces emotional decision-making

-

Improves real-life outcomes

Because returns only matter if you can stick through the drawdowns.

What drawdowns mean for a portfolio?

What drawdowns mean for a portfolio?

When you run a single strategy:

-

Your portfolio is exposed to one type of risk

-

One bad regime can cause a large drawdown

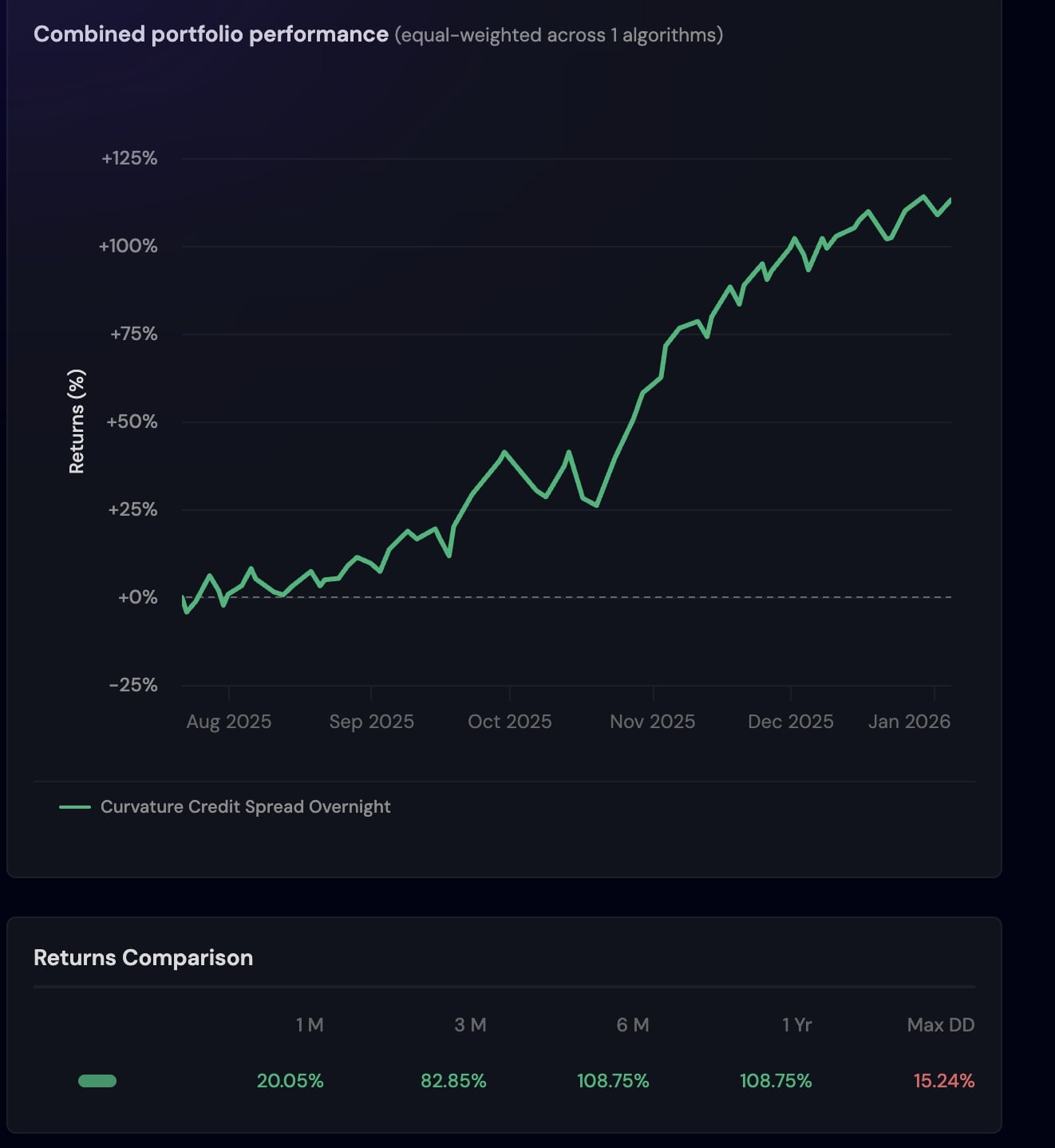

This is why even good strategies can look uncomfortable in isolation. You can see below that max drawdown is around 15% when you have a single algo in your portfolio

How combining strategies helps reduce drawdowns?

How combining strategies helps reduce drawdowns?

This is where portfolio construction matters.

When you combine:

-

Multiple algos

-

With low or moderate correlation

-

Different logic, signals, and market dependencies

What happens:

-

Losses in one strategy are often offset by others

-

Equity curve becomes smoother

-

Drawdowns reduce in depth and duration

![]() More uncorrelated strategies ≠ more risk

More uncorrelated strategies ≠ more risk

![]() More uncorrelated strategies = better risk distribution

More uncorrelated strategies = better risk distribution

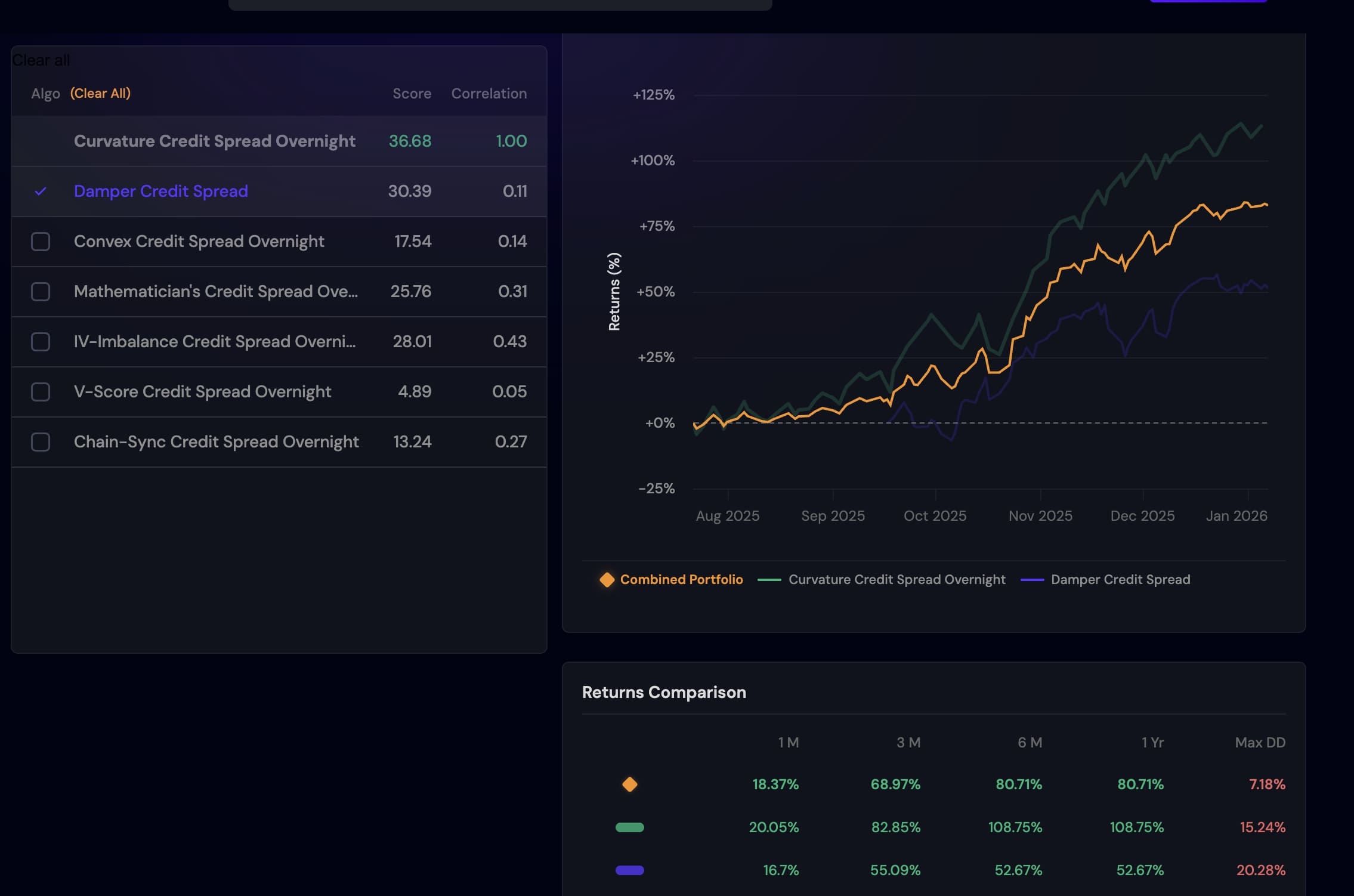

Now you can check correlation among different algos on Stratzy, you can see how allocating into 1 low correlated algo brings down the drawdown by 50%

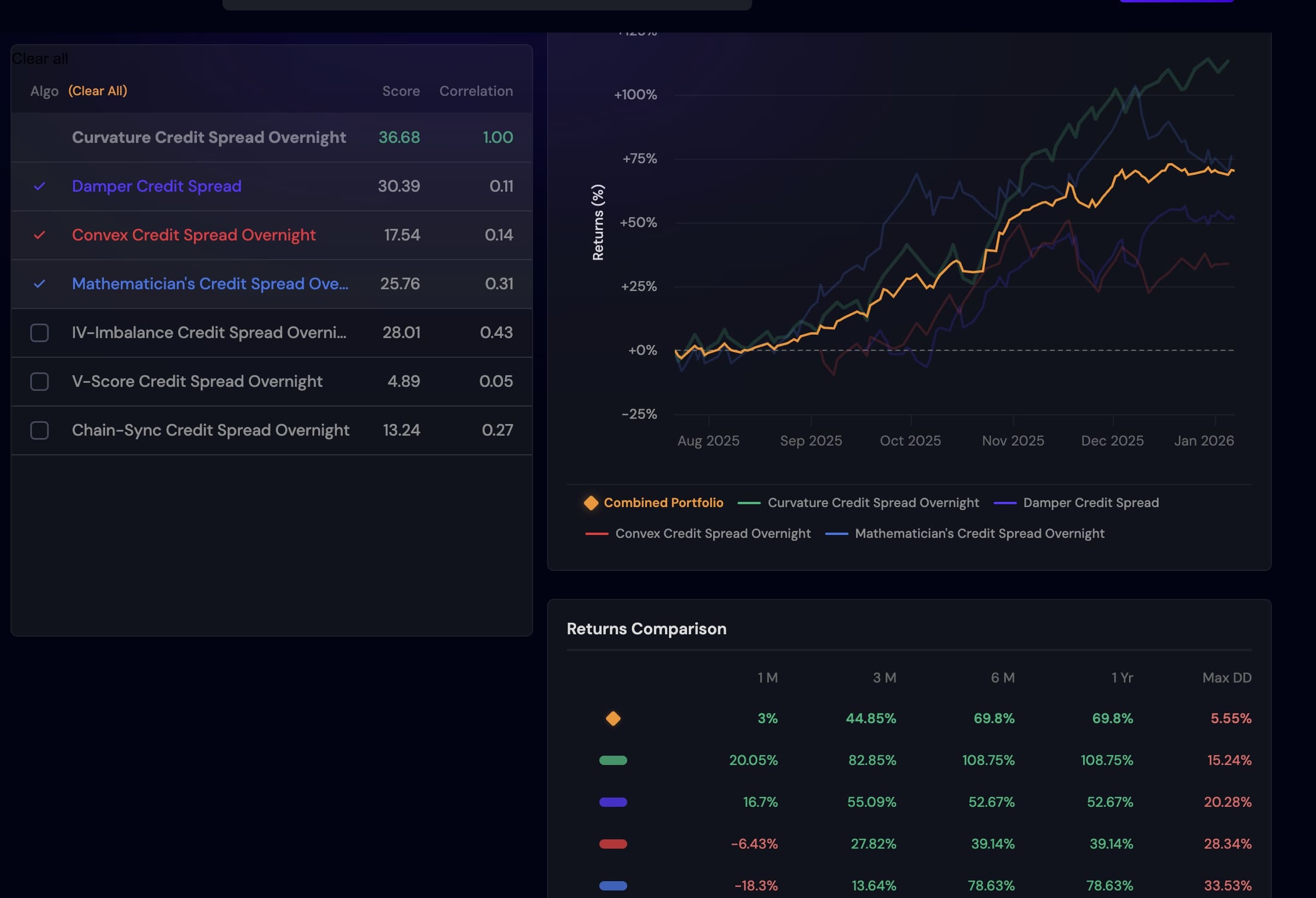

And as we diversify among more low correlated algos it brings down the drawdowns substantially

That’s why:

A portfolio of strategies usually performs better than any single strategy alone not by increasing returns, but by controlling drawdowns.

Final takeaway

-

Drawdowns are unavoidable

-

They are a feature of markets, not a bug

-

The goal is not zero drawdown, but manageable drawdowns

-

Diversification across uncorrelated strategies is one of the most effective ways to achieve this

If returns are the reward,

![]() Drawdown is the price you pay to earn it.

Drawdown is the price you pay to earn it.