This is one of the most asked questions in our community. The honest answer is: it depends. But here’s a framework to think about it properly.

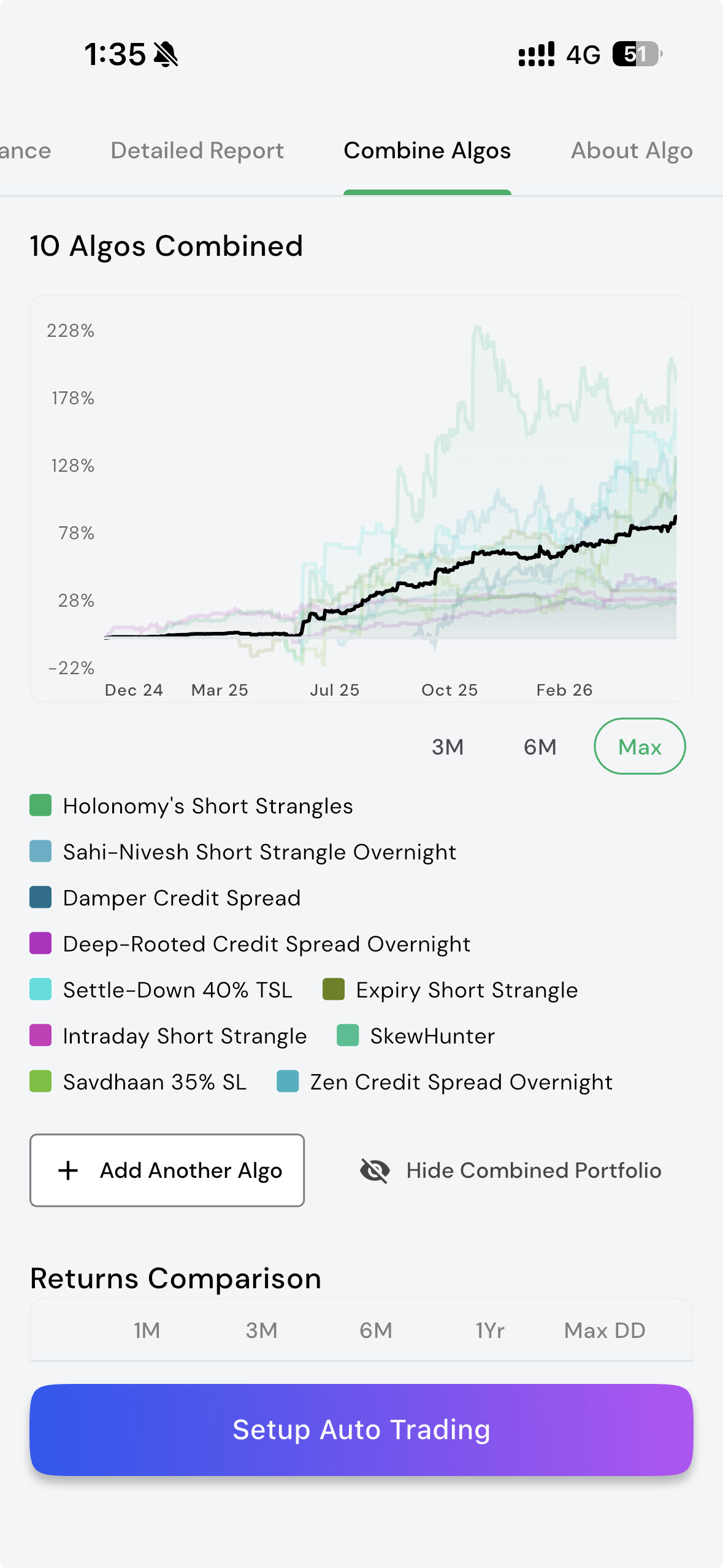

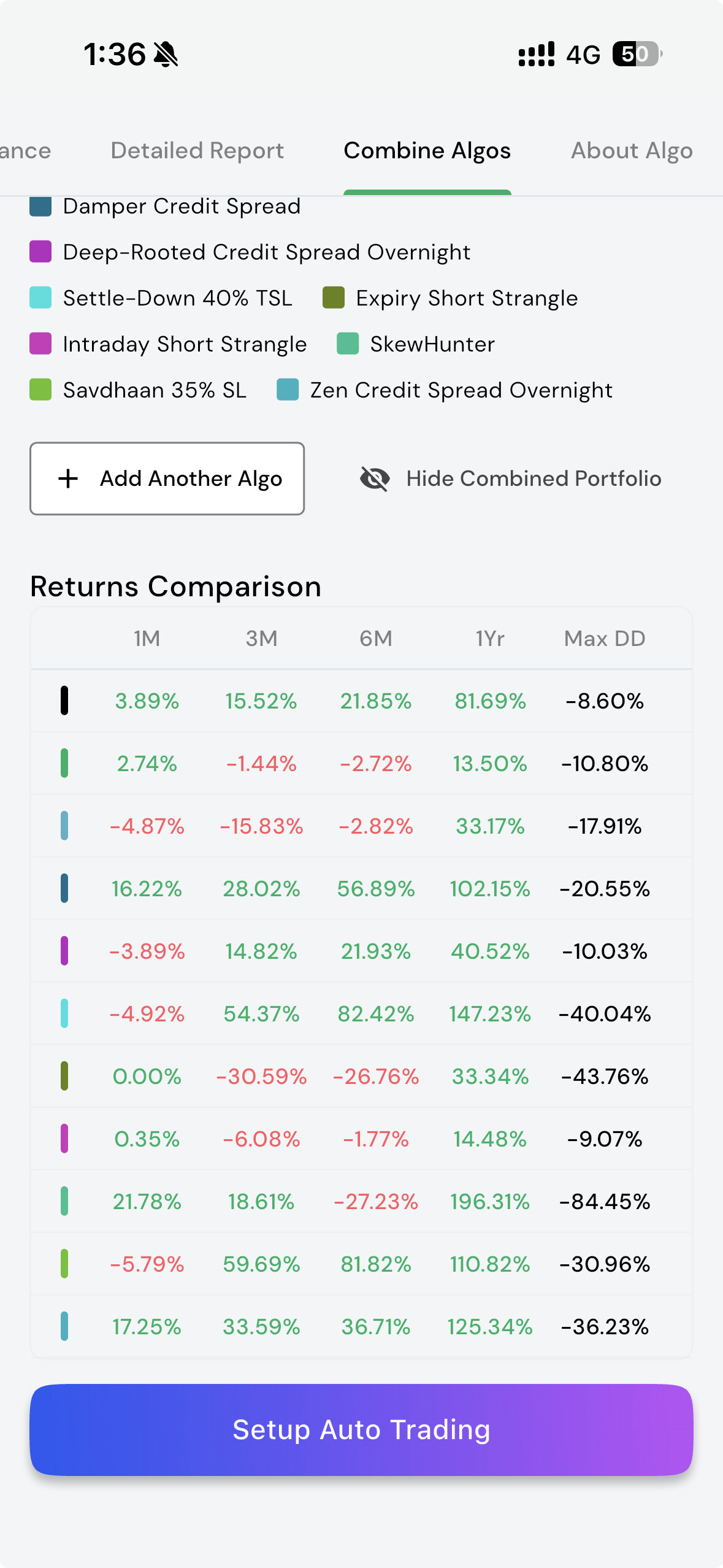

The big idea: more uncorrelated algos = more stable returns

WorldQuant — one of the world’s top quantitative hedge funds — manages $15–16 billion using millions of individual alphas (their term for small, rule-based signals). Not one big strategy. Millions of tiny, uncorrelated ones working together.

The reason? No single algo is right all the time. Markets shift — between trending and sideways, volatile and calm, risk-on and risk-off. When you run many uncorrelated strategies, the ones that aren’t working stay quiet while the ones suited to the current regime do the heavy lifting.

Renaissance Technologies, another quant legend running the Medallion Fund, operates on the same principle — thousands of uncorrelated signals, no single bet dominates the portfolio. Their annualised returns before fees were reportedly above 60% for decades. The edge isn’t one great algo. It’s *diversification at the strategy level.

*

A real example closer to home

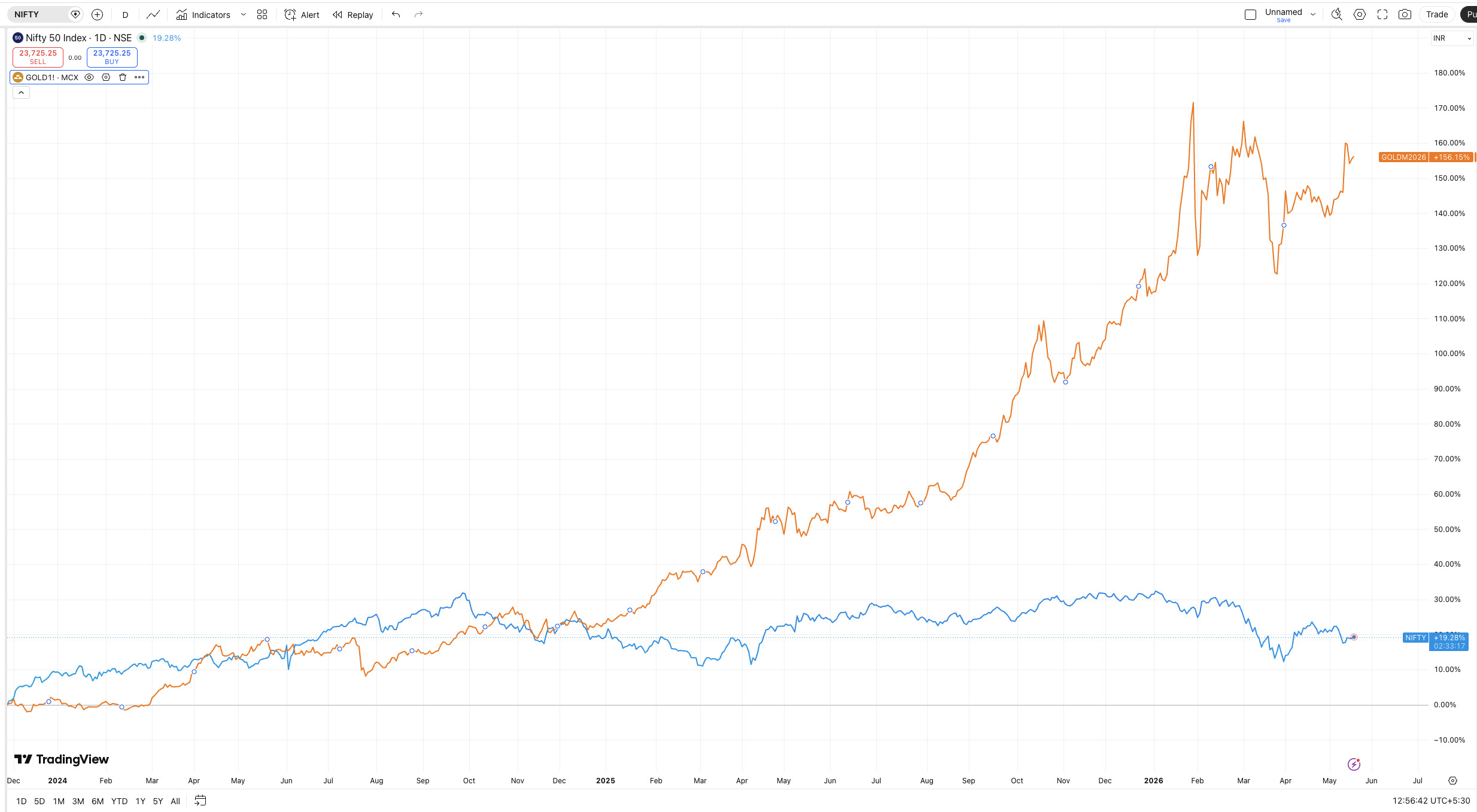

Over the last 2 years, Nifty has been largely flat — consolidating in a broad range. A trader running only Nifty-linked directional strategies would have had a frustrating two years.

But during the same period, gold rallied significantly — up nearly 30–40% — driven by global uncertainty, dollar weakness, and safe-haven demand. Someone running algos across both equity and commodity-linked instruments would have had a much smoother ride. That’s uncorrelated diversification in action — and you don’t need $15 billion to apply it.

Capital tiers — a practical framework

₹15K – ₹2L · Starting out

You can technically start with ₹15–20K, but you’ll only be able to run one algo at a time — no diversification benefit. ₹1.5L–2L is the real starting point because it allows you to deploy 2–3 uncorrelated algos together, which is where the equity curve starts to smoothen.

Think of it like starting a mutual fund SIP — ₹500/month technically works, but ₹5,000 gives you meaningful compounding. The principle is the same.

**

₹2L – ₹5L · Intraday only, no overnight risk**

At this capital level, overnight positions carry disproportionate risk — especially with pledged margin. A global news event, an RBI surprise, or a gap-down open can wipe out days of gains before you can react. Keep it fully intraday.

Algos well-suited to this range:

Damper credit spread – Holonomy short strangle – Fixed RR – Skewhunter

Goal: stay fully intraday, keep margin requirements lean, and compound steadily without overnight exposure.

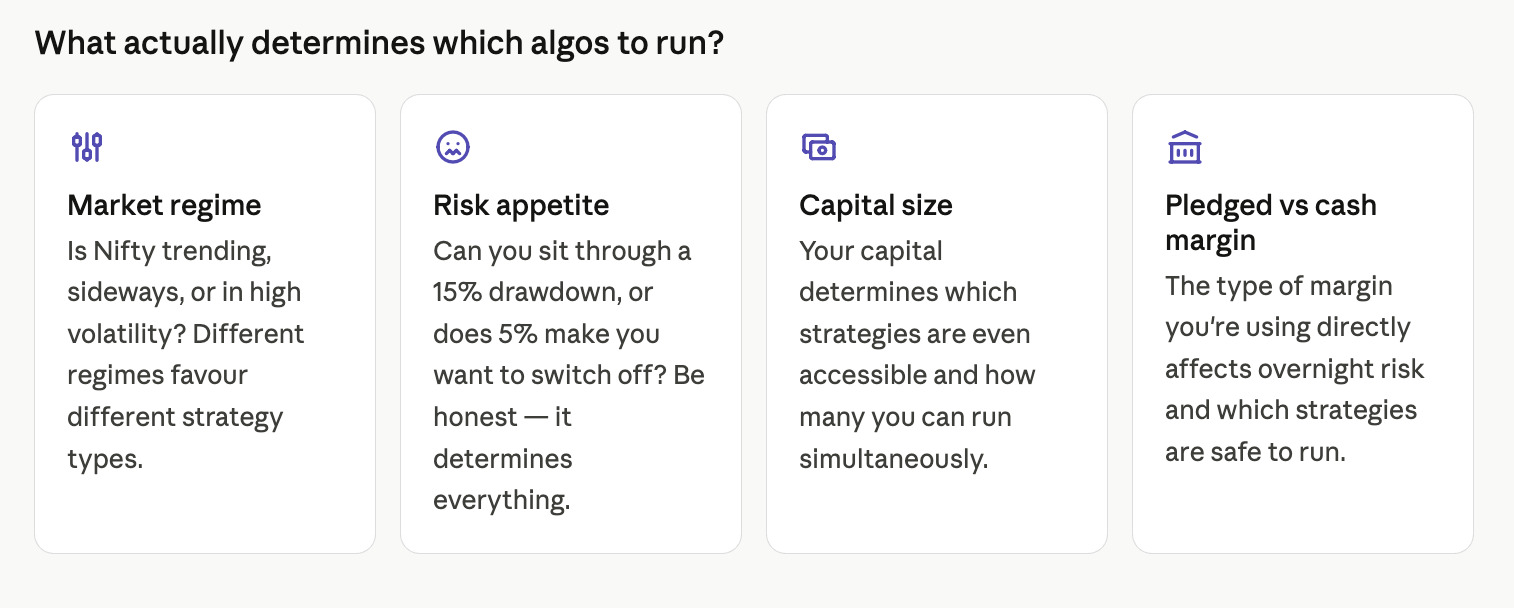

₹10L+ · Regime-based deployment

At this level, capital alone stops being the constraint — market regime becomes the primary input. Think of it like how large funds adjust their book based on macro conditions. You’re doing the same, just at your scale.

50–60% Non-directional — straddles and strangles. Works best when markets are range-bound and IV is elevated but not spiking. Theta decay is your friend here.

20–30% Directional — credit spreads — you don’t need to form a view manually. The algos read the regime and take directional exposure automatically when conditions are right.

~10% Options buying — acts as a portfolio hedge. When markets move sharply (like they did in Oct 2024 or during the Covid crash), this allocation pays for everything else.

This is not a fixed formula — it shifts with the regime. In a trending bull market, you’d tilt more directional. In a choppy, range-bound market, you’d tilt more non-directional.

The pledged margin trap — don’t ignore this

Most brokers recommend a 50:50 split between cash and pledged margin — and for good reason. If your portfolio is pledged and markets move against you intraday, your available margin can drop sharply and trigger auto-square-offs before you even notice.

If you’re running 70:30 or 80:20 (cash to pledged), your actual deployable margin for overnight or margin-intensive strategies is lower than it looks on paper. Size accordingly.

The hidden cost of overnight positions on pledged margin

When you carry overnight positions using pledged margin, brokers charge an interest on the funding — typically 18–24% per annum (varies by broker). That sounds small daily, but it compounds quickly.

Quick math:

Overnight position using pledged margin ₹5,00,000

Interest rate (approx.) 18% p.a.

Daily interest cost**~₹246/day**

Monthly drag on your P&L**~₹7,500/month**

Your overnight algo needs to beat this cost before it starts actually making you money. This is one of the key reasons we recommend staying fully intraday until you have sufficient cash capital — the interest drag silently eats into returns, especially during flat or mildly profitable months.

The takeaway: You don’t need to be a HedgeFund. But you can apply the same principle — run multiple uncorrelated strategies, let each do its job in the right regime, and never bet everything on one approach. The edge in algo trading isn’t any single strategy. It’s the system around them.

Have questions about your specific capital situation or which algos make sense for you? Drop them below, I’m happy to go deeper.