Someone asked a question in our community that deserves a full answer — not just a reply. Because it’s a question many of you have had, even if you haven’t asked it out loud.

The honest answer: Yes. Absolutely. And this is one of the most important concepts in quantitative trading. It’s called alpha decay — and every serious fund in the world is fighting it every single day.

What is alpha decay?

Alpha is the edge a strategy has over the market. When a strategy is discovered and deployed by a small number of traders, it works well — the edge is intact. But as more capital chases the same pattern, three things happen:

1. The strategy competes with itself

When hundreds of algos look for the same signal, they all try to enter at the same time. Prices move before the entry is complete. Slippage increases. The fill you got 6 months ago at ₹45 now costs ₹52. The edge shrinks with every new participant.

2. The market adapts

Markets are not static. When a pattern is exploited consistently, other participants — institutions, HFTs, other algos — start to anticipate and front-run it. The pattern that generated alpha starts generating noise. What worked for 3 years quietly stops working over the next 6 months.

3. Every strategy has a capacity ceiling

Beyond a certain deployed capital threshold, a strategy simply cannot absorb more without degrading its own performance. This ceiling varies — some strategies handle ₹10 Cr, some ₹100 Cr, some only ₹1 Cr before performance starts slipping. The capacity is finite. Always.

The world’s best funds live this problem every day

Renaissance Technologies — Medallion Fund

The most successful hedge fund in history — 66%+ annualised returns before fees for decades. Yet it is closed to outside investors. Why? Because the strategy’s capacity is finite. Opening it to more capital would degrade performance. Renaissance knows this — so they run it only for employees and keep it capped. More money would actually make it worse.

WorldQuant — The alpha factory model

WorldQuant manages $17B+ not through one strategy but through millions of small, uncorrelated alphas. Their entire model is built on the assumption that every alpha decays — so you need a relentless pipeline of new ones. They have entire teams whose only job is to discover the next alpha before the current ones fade.

They don’t try to make one strategy last forever. They build the machine that keeps generating new ones.

Two Sigma — Data-driven alpha renewal

Two Sigma constantly retires old strategies and deploys new ones. Their research team is as large as their trading team — because finding new alpha is as important as running existing alpha. They treat strategy development as a continuous process, not a one-time exercise.

We hear you — and this is exactly why we won’t stop

Over the past few weeks, many of you have pushed back on us in the community and in Telegram. “There are already 100s of algos — why add more confusion?” “New algos will just bump up prices of bundled packages.” “Ab aur confusion ki kya deploy kare.” “Over crowding algos.” We’ve seen every message. We’ve read every screenshot. We haven’t ignored a single one.

And we completely understand where this frustration is coming from. More algos without better discovery, better guidance, and better tooling is just noise. We acknowledge that. We are learning as a company — every piece of feedback shapes what we build next. But here’s what we want to be honest about: algos are and will remain our primary focus. Features, UI, bundles, updates — all of that is important and we are working on it. But the alpha pool is non-negotiable. Because as we explained above, every alpha has a capacity and every alpha decays. The day we stop building new algos is the day we start becoming irrelevant. We’d rather get the feedback and keep building than stop building to avoid the friction.

We also know some of you want better trade updates — knowing when a trade triggers, when it exits, how the algo is performing week on week. That’s a fair ask and it’s on our roadmap. We are adding everything necessary. Just not all at once. Bear with us.

This is the reason we are building India’s largest alpha pool

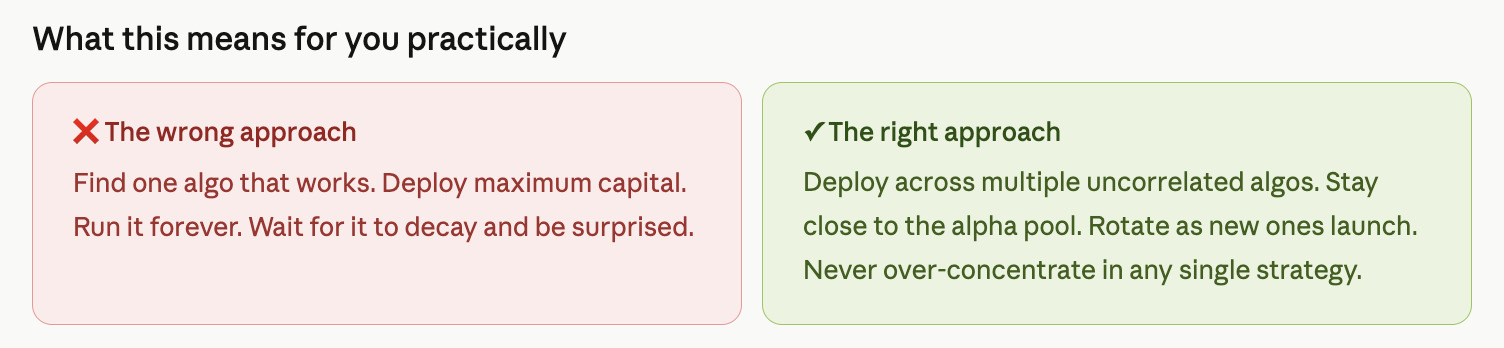

Our goal is not to have 10 perfect algos. Our goal is to build a continuously expanding library of uncorrelated strategies — because:

- Every alpha has a capacity — when one approaches its ceiling, the next one needs to be ready

- Every alpha decays — markets adapt, patterns get front-run, edges erode over time

- More uncorrelated algos = smoother equity curves = better risk-adjusted returns for every member deploying here

- The community that deploys across the widest alpha pool has the most durable edge — not the one sitting on the fewest strategies

India’s algo trading industry is still in its first chapter

Here’s something worth putting in perspective. In the US, top hedge funds use satellite data to track the number of cars in Walmart parking lots — to estimate footfall before quarterly earnings come out. They track oil tanker movements via satellite to predict crude supply weeks before official data. They analyse credit card transaction data from millions of users to estimate consumer spending before any government report is published. This is the level of alternative data and alpha infrastructure that exists in developed markets.

In India, we don’t have any of that. NSE data access is limited. Alternative data infrastructure barely exists. Regulatory frameworks around algo trading were formalised only in 2025. Most retail traders didn’t even know what an algo was three years ago.

We are extraordinarily early. The entire Indian algo trading industry is in what the US was in the late 1990s — before quant funds became mainstream, before alternative data became an industry, before systematic trading became the dominant force in markets.

This early stage is exactly the opportunity. The traders who build systematic habits now — who understand alpha, capacity, regime-based deployment, and portfolio construction — will be structurally ahead of everyone who is still typing “Ce” in the RBI Governor’s chat five years from now. We’re not just building algos. We’re building the community that will define how India trades systematically. That takes time. That takes more algos, not fewer.

Conclusion

The game is not to find one perfect strategy and hold it forever. The game is to keep chasing alpha — systematically, continuously, across different market conditions and structures. That’s what the world’s best quant funds do. That’s what we’re building here. And that’s the real answer to Kishor’s question.

Have you thought about capacity limits when deploying your algos? Do you actively rotate across strategies as new ones launch? Drop your approach below ![]()